Saving Corporate M&A (Part 3) - Intent Over Volumes

Tips for running corpdev better

Last week’s post was about hype cycles and how making these the central to your investment case can be harmful. You can read more on that below -

Saving Corporate M&A (Part 2) - Hype & Relevance

Thank you for tuning in. Last week’s post was about understanding how businesses do disservice to themselves by taking an “opportunistic” stance in M&A and losing out on buying high quality businesses when the opportunity actually comes. You can read more here -

Resuming the series, this week, let’s take a look at some of the poor practices that creep into deal evaluation and execution from time to time and what should be done instead.

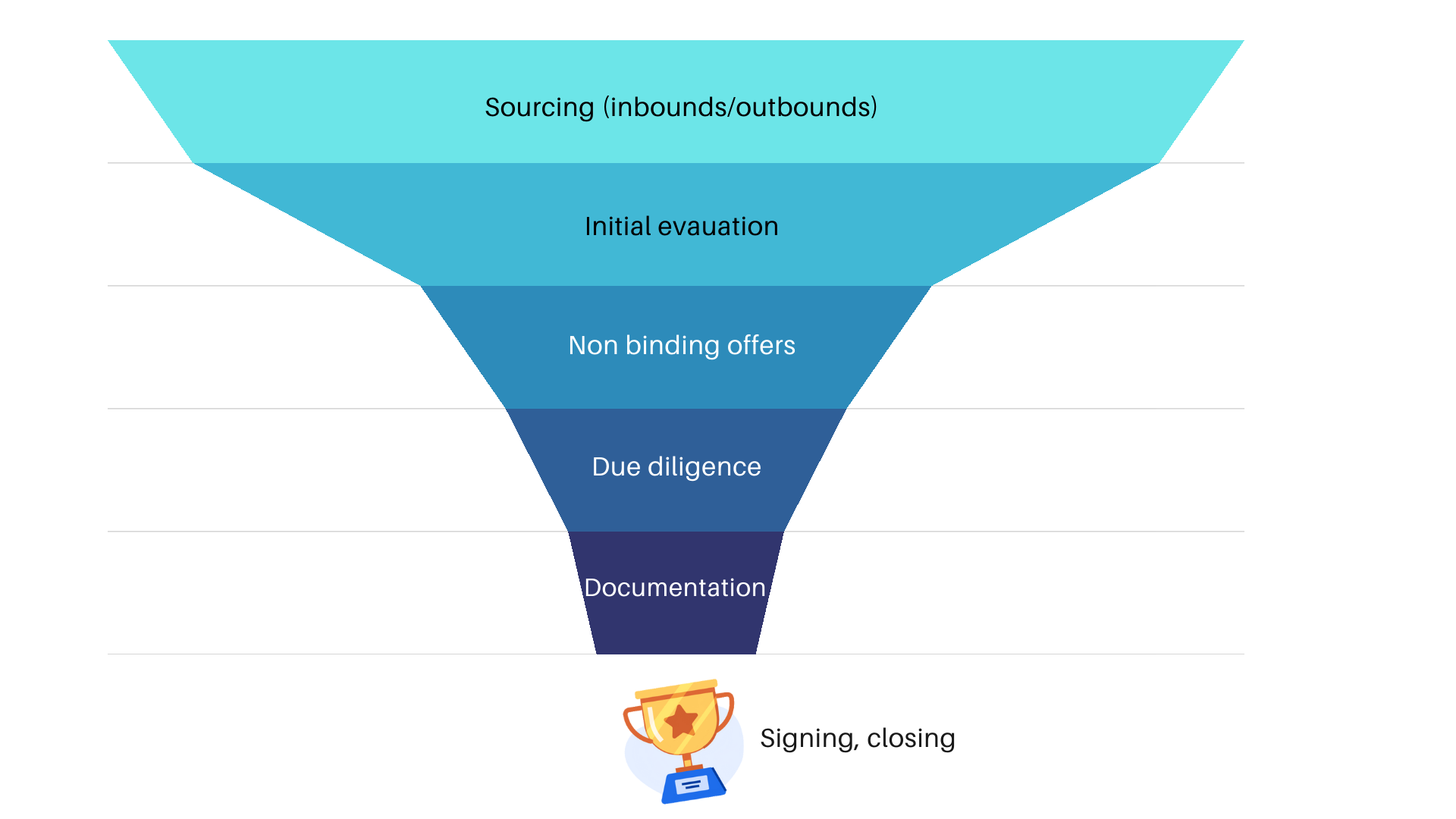

The usual deal funnel looks something like this below, with the various stages that a deal goes through. Successful deals will cross each stage and get to the signing stage, while the rest will drop off at intermediate stages. Deal drop-off is high in the first two stages and then it peters down.

As you run through the deal process, you often end up allocating a large chunk of time and other resources towards the early stages, given the sheer number of deals in the early stages. Your allocation could look something like this -

Sure, you do have to allocate fair and adequate attention to deals at each stage of the funnel, but in the real world, you cannot ignore time and resource constraints, and more attention to the early stages naturally implies less attention to the later stages. Later stages matter much more when it comes to the success or failure of deals. The harm or loss of opportunity from letting go of a good acquisition is hypothetical*, but the resulting harm from making a poor acquisition is real.

More time spent in diligence can bring out more blind spots and negatives (or even positives) in a deal. More time spent in making the offer or in documentation can allow for better structured deals with more scenarios covered, more robust valuation and so forth.

While there is no formula at hand to help you perfectly allocate your time and resources across the various deal stages, there are some very simple principles that can really help you out -

Deal making is a series of noes, until you have no more noes to say. And for each deal that happens, there are several that don’t

The earlier you say no, lesser the time and effort that is sunk/lost

Having a reliable system to say no quickly will help free up time in the early stages and in turn give you more time for the more crucial later stages

Having a clear M&A strategy - what areas to expand into inorganically, what kinds of businesses to acquire - by business model, segment, geography, stage. etc. is halfway to having a quick and reliable system to assess the target’s fit with the acquirer

Anything that is not a good fit should be avoided. It does not matter how attractive the price or other terms may be

And when you have an attractive opportunity, go for the kill. It makes little sense to progress a deal far into the pipeline only to lose it for lack of timeliness or boldness in your bid

Happy deal making!

*in tech, lost deals can also lead to terrible consequences, including loss of relevance and inability to counter disruption, but for this post, lets assume only hypothetical impact in case of lost deals.